The International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker has released preliminary data indicating a 14.6% decline in global smartphone shipments to 268.6 million units in the first quarter of 2023 (1Q23).

This represents the seventh straight quarter of decline as the market suffers from low demand, inflation, and financial uncertainties. Previously, IDC estimated that worldwide smartphone shipments would decrease 1.1% in 2023.

Market Continues to Struggle

While the decline is more than the 12.7% IDC had previously forecasted, it is not surprising. Inventory levels have remained elevated across regions, but have improved compared to six months ago, thanks to reduced shipments and heavy promotional activities.

The industry is currently experiencing a period of inventory clearing and adjustment, as market players deploy a conservative approach rather than dumping more stock into channels to chase temporary gains in share.

Cautious Approach by Market Players

According to Nabila Popal, research director with IDC’s Worldwide Tracker team, market players remain cautious, deploying a conservative approach, as they want to avoid an unhealthy situation like in 2022. Popal suggests keeping a close pulse on the market, as anyone who jumps in too soon will drown in excess inventory.

The market is expected to cross into positive territory in the third quarter and see healthy double-digit growth by the holiday quarter, barring unforeseen elements.

Double-Digit Declines in Almost All Regions

Almost all regions suffered double-digit declines in 1Q23. China witnessed a close to 12% drop, which was slightly more than expected despite the recent reopening of the market. Consumers are favoring travel and entertainment over smartphone shopping, and uncertainty still continues, reducing consumer mood.

Developed markets, like the USA and Western Europe, coped better than others with declines of 11.5% and 9.4% respectively. Emerging markets, like APeJC, CEE, and MEA, saw bigger declines ranging from 17% to 20%.

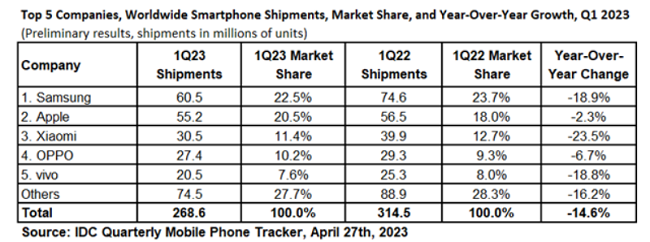

Worldwide Smartphone Shipments, Market Share, and Year-Over-Year Growth, Q1 2023 by IDC

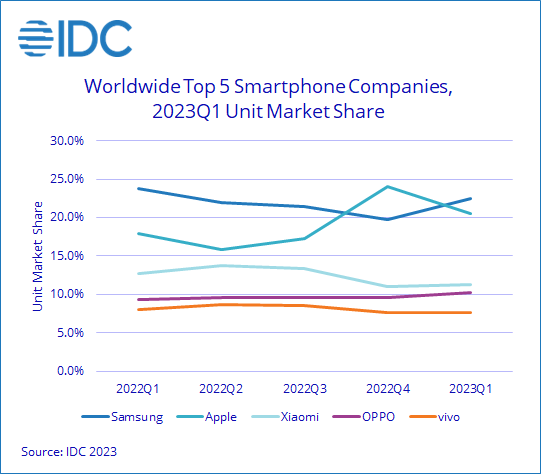

The International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker has released preliminary data on worldwide smartphone shipments, market share, and year-over-year growth for Q1 2023. The data shows that Samsung maintained its position as the market leader, followed by Apple, Xiaomi, OPPO, and Vivo, respectively. Other smartphone makers collectively hold the remaining market share.

- Samsung led the smartphone market in Q1 2023 with 60.5 million units shipped and 22.5% market share.

- Apple followed closely with 55.2 million units and 20.5% market share.

- Xiaomi ranked third with 30.5 million units and 11.4% market share.

- OPPO came fourth with 27.4 million units and 10.2% market share.

- Vivo rounded out the top five with 20.5 million units and 7.6% market share.

- The rest of the market accounted for 74.5 million units and 27.7% market share.

Commenting on the report, Ryan Reith, Group VP with IDC’s Worldwide Tracker team, said:

We are encouraged by the recent conversations we had with OEMs and supply chain partners who indicate that the smartphone industry is collectively hopeful that we will witness a recovery by the end of this year and into 2024. The main reason for the sharp decline in supply in the past few months was the brands that target the low to mid range segment of the market.

This is usually where the competition is fierce and the profits are slim. Normally, these players are more reluctant to resume production, and while this might still be true, we are beginning to see evidence that this group is becoming more optimistic.